Vietnam's Strengths & Struggles

Why some of the shine came off a Southeast Asian success story

Vietnam is having a moment. The Southeast Asian nation has firmly established itself as an economic dynamo: posting GDP growth consistently northward of 6% per year, hoovering up vast inflows of foreign investment dollars, and birthing an expanding class of urban, middle-class consumers. Over the past two decades, few countries—either in East Asia or further afield—have outperformed that trajectory. In short order, Vietnam’s roughly 100mn-strong population has gone from abject poverty to citizens of a solidly middle-income, globally integrated export powerhouse.

The World Bank lays out Vietnam’s success in no uncertain terms:

Vietnam has been a development success story. Economic reforms since the launch of Đổi Mới in 1986, coupled with beneficial global trends, have helped propel Vietnam from being one of the world’s poorest nations to a middle-income economy in one generation. Between 2002 and 2021, GDP per capita increased 3.6 times, reaching almost US$3,700. Poverty rates (US$3.65/day, 2017 PPP) declined from 14 in 2010 to 3.8 percent in 2020.

As does this graph from World Economics:

Source: World Economics

So there you have it: internal marketization reforms, working in conjunction with a broadly favorable external environment defined by geopolitical stability, generous FDI flows, and trade openness, go a long way in explaining Vietnam’s explosive economic take-off. Now of course with breakneck development and greater integration into the global supply chain comes heightened attention and scrutiny. Perhaps the single biggest piece of context framing a lot of the focus on Vietnam right now—at least among outside observers—is the ongoing US-China trade and technology fracas. With the two superpowers going through a long and tumultuous process of selective decoupling (to say nothing of China’s rising production costs and darkening internal picture), many multinationals have embraced “China+1” strategies aimed at scaling back their reliance on the People’s Republic.

Against the backdrop of those frothy geopolitical dynamics, Vietnam’s core advantages—geographic centrality, inexpensive labor, youthful population, relatively open business environment, and political stability—have established it as a critical linchpin (and China alternative) in supply chains spanning electronics, apparel, and automobiles. Reflecting growing multinational interest, inbound FDI flows in 2022 hit a whopping $22.4bn—the highest level in over a decade—and The Economist proclaimed last Fall that Vietnam “is emerging as a winner from the era of deglobalization.”

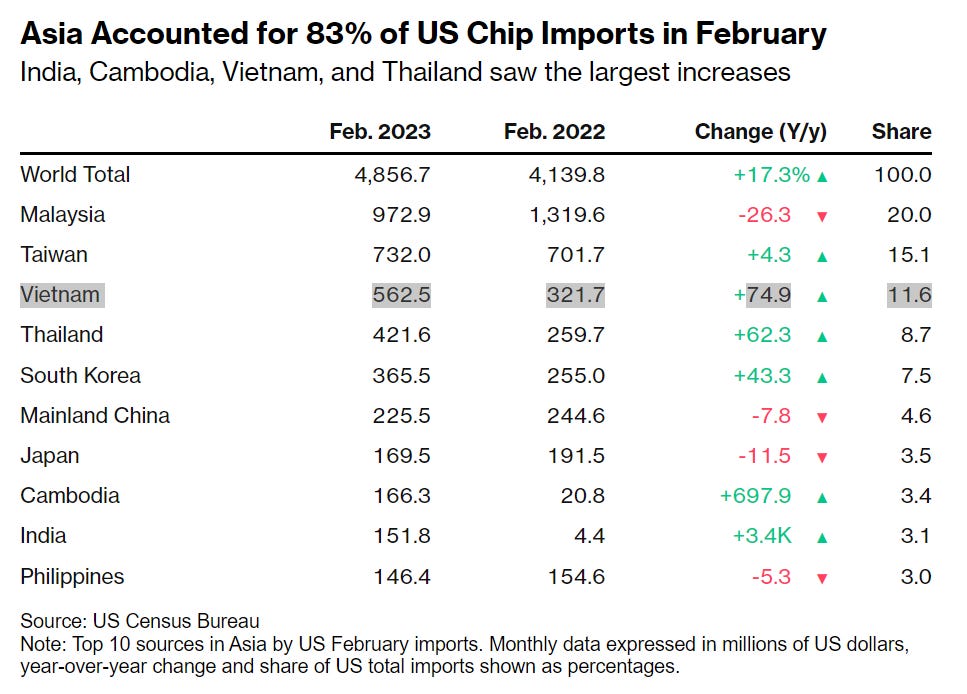

Vietnam’s growing centrality cannot be overstated: as one prominent example, data suggests it’s now the third-largest exporter of microchips to the US, trailing behind only Taiwan and Malaysia, after “revenues swelled by 75 percent year-on-year, reaching US$562 million in February 2023.”

Source: Bloomberg

Some very notable multinationals, including Samsung, Foxconn, Intel, Quanta, and Keppel have led the charge—pouring in dollars to affirm support for Vietnam as a potent manufacturing base for a growing share of electronics and digital supply chains, an outpost for R&D, and a lucrative consumer market unto itself.

That all sounds quite promising, but it’s only part of the story. Of late, some notable cracks have emerged in the narrative. Warning signs are stirring unease amongst foreign multinationals and Vietnam’s burgeoning business class alike.

So what’s going on?

On one level, a lot of the current headwinds hinge on the vicissitudes of a highly integrated global marketplace. Vietnam ranks as one of the world’s most trade-dependent economies, and, as such, remains captive to developments outside Hanoi’s control. A confluence of external factors— interest rate hikes, supply chain snarls, China’s weaker-than-expected growth numbers, and slumping export orders in key areas like apparel and electronics—have undercut Vietnam’s post-COVID bounce. To wit: while growth surged 8.0% in 2022 on the back of the post-pandemic reopening, this year’s GDP figures show a notable taper—coming in at 3.3% in Q1 and 4.14% in Q2.

Source: Nikkei

That’s created perilous ramifications for a segment of Vietnam’s industrial workforce. The tech-focused Rest of World publication lays out those dynamics, and their blowback for ordinary factory workers, in an illuminating piece of recent reporting:

These are the symptoms of a global slump in the demand for electronics, and the result of difficulties in sourcing components from China. Once the pandemic’s peak began to decline, people in the U.S. or Europe tamped down on their purchases of new smartphones and TVs; when inflation bit, they tightened their belts another notch. New orders and production for big electronics companies tanked to their worst levels since mid-2020. The effects of that contraction have rippled across the world, throwing the lives of tens of thousands of people who make these items into disarray.

In the first five months of 2023, 45,000 people lost jobs in electronics manufacturing in Vietnam. The country’s biggest company, Samsung, which once offered lucrative pay that was a worker’s dream, is now slashing work hours, renewing fewer contracts, and furloughing some workers, current employees told Rest of World. Dorms that housed employees assembling smartphones and Apple Airpods stand half-empty. According to workers employed in these factories for up to a decade, this is the worst slump in their memory.

Nor is the fallout confined to manufacturing orders. Tourism—a significant growth driver in the domestic service sector—remains far below pre-pandemic levels. Perhaps more problematically still, rising capital costs have brought an end to the easy money that’s underpinned Vietnam’s startup ecosystem; ushering in what’s been described as a venture capital “funding winter” across Southeast Asia that’s imperiling company valuations and hamstringing Hanoi’s aspirations to build out a vibrant digital economy. The Vietnamese government aspires to see digital services comprise 20% of the overall economy by 2025.

Critically though, this isn’t just a story of external vulnerabilities. I want to home in here on some of Vietnam’s self-inflicted challenges.

Energy and grid: Vietnam's start to the summer proved to be an unusually brutal one. In June, extreme heat levels smashed previous records across SE Asia; prompting authorities to turn off streetlights, ration electricity, and ask factories operating in the north of the country to scale back their energy usage by as much as 50%. As Reuters wrote at the time, while Vietnam “has nearly 80 gigawatts (GW) of maximum installed power capacity,” June’s heat stress “cut output to less than half that at peak times.”

To be clear, extreme heat is not a uniquely Vietnamese problem. However, this summer has brought to a head the challenges Hanoi faces in managing an escalating climate crisis while simultaneously ensuring a reliable supply of power to support the country’s industrial base.

A couple of points here:

Average peak energy demand volumes have (unsurprisingly) surged roughly 4x over the last 20 years, creating new strains on consumers—households and industry alike.

Climate change, heat stress, and rising sea levels present a monstrous basket of problems over the short, medium, and long term: lower agricultural productivity, worsening health outcomes, and (potentially) millions at risk of coastal flooding given the concentration of Vietnam’s population in low-lying coastal areas. As the UN puts it, the country “faces potentially significant social and economic impacts across multiple regions and sectors. Without effective adaptation and disaster risk reduction efforts multidimensional poverty and inequality are likely to increase.”

Vietnam remains heavily reliant on coal (which supplies about 60% of electricity output) and other hydrocarbons for its energy profile. While Vietnam’s grid is straining beyond capacity, much-overdue reforms to the electricity market remain bogged down by bureaucratic infighting, structural barriers, special interests, and general inertia.

The clean energy drive remains behind schedule, with underutilized capacity in both solar and wind. Authorities have so far struggled to unlock the roughly $15.5bn in UN funding for their post-coal clean energy efforts due to bureaucratic turf wars.

All of this matters quite a bit. Vietnam’s industrial potency isn’t simply a story of inexpensive labor costs; to keep the good times rolling, the state must deliver an array of public goods—both tangibles like roads, ports, and power systems, and less tangibles like political stability, a reliable business climate, and sound economic management—to sustain its allure as a rising manufacturing power.

Few things are more disruptive to the operation of industry than blackouts and supply cuts—especially when they pressure the operations of foreign MNCs while exposing the bureaucratic and structural deficiencies of Vietnam’s coal-intensive energy profile. Looking ahead, an inability to resolve the power supply issue may act as a critical growth impediment.

Anti-corruption and paralysis: adding an extra layer of political risk into the equation is that Vietnam’s power struggles are not simply about energy supply and grid quality. Vietnam, much like its gigantic northern neighbor, operates as a tightly controlled authoritarian party-state. Power is uniformly concentrated in the hands of the ruling Vietnamese Communist Party (VCP).

The parallels continue. Much like in Xi Jinping’s China, for the past six years the VCP’s elderly General Secretary, Nguyen Phu Trong, has been spearheading a comprehensive, anti-corruption crackdown that’s ensnared high-ranking political officials and upended business as usual. Given the opaque nature of Vietnamese elite politics, it’s hard to discern whether the underlying motivation behind the campaign, dubbed “Blazing Furnace,” is rooted in a genuine desire to stamp out corruption and improve the overall business climate, simply a mechanism for political score-settling, or some combination thereof. Regardless, the net result has been unambiguous: a climate of fear and administrative paralysis has taken hold that’s locking up regulatory approval and government procurement processes.

Analyst Steven Westervelt writes that “whatever the motivation behind it, ‘blazing furnace’ has led to many officials sitting on their hands, apparently fearing that any mistake they make may be pounced upon by either those seeking to get them out of the way or overzealous investigators wanting to boost numbers of arrests.”

It’s important to note here that foreign multinationals have been largely spared from the state’s wrath. However, the anti-corruption campaign is exacerbating woes in the all-important property and construction sectors— where domestic firms struggle to raise capital, secure loans, and advance big-ticket projects.

Now, to be clear, there are myriad factors at play in assessing the current state of Vietnam’s real estate sector—encompassing broader economic weakness, liquidity concerns, missed bond payments from major development groups, stringent reporting requirements, and falling property sales as potential buyers put off purchases. Nonetheless, the anti-corruption drive is clearly biting into market confidence. Here’s the FT:

In a sign of the economy’s sensitivity to the property sector, the arrest last year of tycoon Truong My Lan, chair of Van Thinh Phat Holdings, sparked a run on Saigon Commercial Bank until the country’s central bank intervened to reassure depositors.

The tumult set off a fire sale of Vietnamese real estate bonds, many of which fell deep into distressed territory. Hundreds of smaller developers and property groups were forced into bankruptcy, and thousands of projects were suspended.

Staying Bullish

I don’t want to overstate the pessimistic case. Yes, Vietnam will almost assuredly remain a security-obsessed authoritarian regime for the foreseeable future. Its bureaucracy will remain cumbersome and reform-resistant in key areas that will undoubtedly upset the business class. Property woes will also likely remain barring systemic reforms. The China parallels—information crackdowns, a paralyzing anti-corruption campaign, weakness in the real estate market, declining export orders—are quite notable, but only to a point. Unlike China, I remain broadly bullish on the SE Asian dynamo over the decade ahead.

Here’s why:

Fundamentals: competitive labor costs, an increasingly well-educated and skilled workforce, and strong growth in capital expenditure—in the form of both FDI and state-led infrastructure investment—are all causes for optimism over Vietnam’s medium-to-long-term growth prospects.

Pro-business: despite the anti-corruption and civil society crackdowns, the VCP has generally maintained an overall pro-growth orientation—proving itself hospitable to the concerns of the international business community. To generalize a bit, Vietnam remains a broadly attractive FDI destination.

Geopolitics: despite periodic griping from US officials over unfair trading practices, Vietnam simply is not (and will not become) a serious great-power rival. Nor will it face anything like the accompanying onslaught of trade and investment restrictions currently unending business as usual over in China. In fact, Hanoi will likely continue to benefit from playing DC and Beijing off one another as the Sino-American decoupling process rolls on and on.

Solid demographics: to be clear, falling birth rates and increasing life expectancy are leading to a rapid aging of the Vietnamese population (which is a serious long-term concern area). However, for the time being, Vietnam's population profile remains comparatively youthful. A large share of workforce participation will allow the economy to benefit from an ongoing demographic dividend as its population moves into urban areas and more productive economic sectors.

Forgive the incoming tangent but I want to focus on one more reason for optimism. Recently I’ve become quite taken with The Atlas of Economic Complexity over at Harvard University’s Growth Lab. The project attempts to measure the—you guessed it—complexity (or know-how) of varying national economies; which it deems a key determinant of economic development. To summarize a bit, the theory undergirding the project’s work holds that those countries that grow quickly and thrive are the ones that successfully deploy their human capital base (read aggregate brainpower) to produce a diverse and complex (read non-ubiquitous) array of products and services. The more complex and varied the products being made by all those aggregate brains, the more likely your country is to be heading in the right direction.

Here’s Harvard Growth Lab director Ricardo Hausmann explaining how it all works on a recent episode of Bloomberg’s Odd Lots podcast:

Economic complexity is an attempt to measure how much countries or places know what to do. So it’s like trying to measure know-how. Now if you want to think about knowledge, you say, “Well, I know people who have a Bachelor's degree, people who are high school dropouts, people who have a PhD.” That sort of tells you how much a person knows. But if you ask yourself, how much does a society know? Well that would be different. That would not be characterized by the average number of years of schooling that the society has. No, a society that is full of just dentists will know less than a society that is half dentists and half lawyers. Or a society that is a third dentist, a third lawyer, a third engineers. So in some sense you want to know how much the whole of society knows.

And one of the important things about knowledge is that knowledge at the societal level has been exploding exponentially. But our mental capacity to know has not. So the way the economy has been adapting and adopting growing amounts of knowledge is by putting different bits of knowledge in different heads. Sort of like parallel processing. You know, if you want to run a company, you'll need somebody who knows about accounting, about finance, about marketing, about human resource management, about contracts, about taxes, about procurement, about engineering. So you want to have a lot of knowledge to run these things, but you cannot stuff that knowledge into a single head. You have to spread it into a bunch of heads and then you have to bring those heads together back again. You have to kind of put Humpty Dumpty back together again. So the way in which a society grows is it grows its knowledge by putting different bits of knowledge in different heads and then by bringing those heads together.

Now if a society makes very simple things, it makes things that can be done by few people because the knowledge that are is needed to make one of those things, you know, fits in just a few heads. But if you are going to do stuff that requires a lot of knowledge, you'll have to bring many, many more of these heads together. You'll have to network these brains together to make that thing. So complexity emerges as the consequence of distributed knowledge in society. You have different bits of people knowing different things and then you have to bring those things together and then these complex networks emerge from that process.

Alright now let’s take a look at how Vietnam fares. The answer? Fantastically well! If you look at the graph below, you’ll notice Vietnam’s position rocketed up 46 spots from a base rank of 107 back in 1995 to 61 in 2021. That outcome is both highly impressive and not terribly shocking given all that FDI inflow, manufacturing diversification, and digital transformation.

Source: Atlas of Economic Complexity

If we put stock in the analytical prowess of The Atlas, then it’s hard not to feel quite bullish! Critically, Vietnam is “more complex than expected for its income level,” which leaves it poised for strong future growth as it “takes advantage of many opportunities to diversify its production using its existing knowhow.” In fact, just last month Hausmann specifically cited Vietnam as a country “that will lead global growth in the coming decade” by virtue of having already diversified its economic production into increasingly complex sectors.

Anyway, that’s my current read on Vietnam. Yes, the country’s economic struggles right now are concerning. Yes, the human rights picture is undoubtedly abysmal. And yes, there are still tons of geopolitical and market variables outside Vietnam’s control that may yet go haywire. Regardless, I don’t think any of those factors should obscure what is likely to be a brighter future in terms of Vietnam’s overall development trajectory and growing centrality to global supply chains.